SECTION 4.1 – PARLIAMENT’S ROLE IN BUDGET EXECUTION & AUDIT/OVERSIGHT PHASES

Overview: In this section, we delve into Parliament’s crucial role in budget execution and oversight.

We will explore why the execution stage is pivotal for monitoring budget credibility, legislative scrutiny of budget implementation, and the role of SAIs in enhancing parliamentary oversight.

Exercise: Review the three videos:

Human Coined Podcast, Ep. 25, 10:00 – 12:52 Here is a clip discussing why budget credibility analysis is important.

Significance of Execution Stage in Ensuring Budget Credibility

Video: What is Budget Credibility

Video: What are the consequences when governments deviate from approved budgets?

Now, reflect and answer the following questions:

Upload your answers in the comment box provided below

Your answers will be shared only with the course facilitator via [email protected]

- What is budget credibility?

- Why is it important?

- How is budget credibility relevant to your organizational mission?

Insert your answers below

Overview of Budget Execution and the Role of Parliament during Budget Execution

Budget execution and budget deviations:

Budget execution begins once the Executive’s Budget Proposal (EBP) is approved.

Citizens can expect the budget approved by Parliament to serve as a ‘roadmap,’ guiding government spending decisions. See this IBP budget credibility factsheet

In practice, budgets are not always implemented as approved. Sometimes, there are good reasons for budget deviations, or instances when actual spending deviates from the approved budget. For instance, governments may revise spending plans in response to changing economic conditions or a natural disaster.

Budget deviations may also result from:

- Unrealistic revenue projections leading to lower-than-expected revenues.

- Weaknesses in Public Finance Management (PFM) systems that make it difficult for the executive to implement the budget as approved (e.g., poor reporting systems).

- Executive mismanagement or corruption ([ibid](https://internationalbudget.org/wp-content/uploads/budget-credibility-fact-sheet.pdf)).

There are two types of budget deviations: (1) underspending, when actual spending is less than what was allocated in the budget; and (2) overspending, when actual spending is greater than what was allocated in the budget (See the IBP Budget Credibility Factsheet

These deviations highlight the importance of maintaining budget credibility, which ensures that the government’s financial commitments are met as intended.

Low budget credibility, when governments do a poor job of meeting revenue and expenditure targets, is a problem that requires the attention of the executive, Parliament, the Parliamentary Budget Office (PBO), SAIs, and civil society.

Budget credibility challenges often have the greatest effect on vulnerable populations and sectors critical for achieving the sustainable development goals (See the IBP Budget Credibility Factsheet).

For example, research conducted by the International Budget Partnership (IBP) has shown that underspending is generally worse in low-income countries and in critical sectors such as agriculture and health. It is also especially pronounced in capital projects targeted for socioeconomic development, such as investments in schools and hospitals.

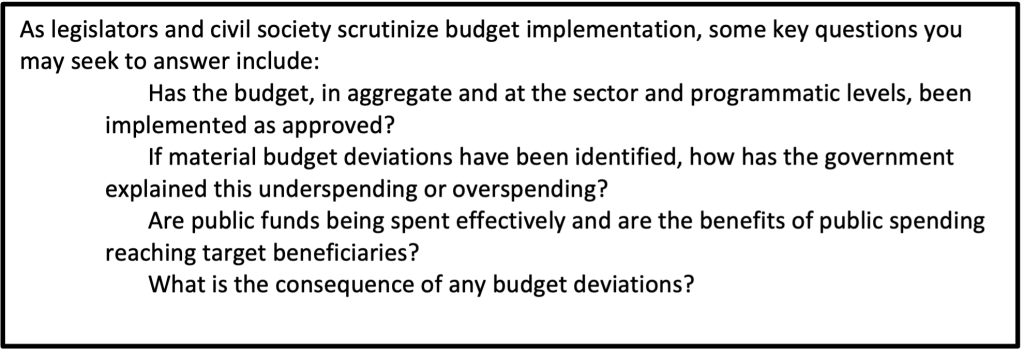

Parliamentary Scrutiny of Budget Execution

While implementing the budget is an executive function, stronger parliamentary oversight during budget implementation can help governments implement budgets as intended, enhancing public’s trust in government to use public resources wisely and deliver on promises reflected in national budgets (IBP 2022:62). Parliaments, especially through the work of parliamentary committees, can engage on the budget during the implementation phase in three ways.

First, parliaments should monitor implementation of the budget, including reviewing In-Year Reports (IYR), produced by the Ministry of Finance (MoF) to compare actual expenditures with approved budget allocations. This enables legislatures to assess whether funds are being spent effectively and for their intended purpose. This oversight function ensures accountability, transparency, and effective use of public funds. Legislative oversight of budget execution typically takes place within parliamentary committees, such as a specialized budget or finance committee. The committee may invite finance ministry officials to respond to questions regarding budget implementation. Good practice indicates that legislatures, in committee, should examine in-year implementation of the budget at least three times during the budget year and publish a report with findings and recommendations (OBS 2024b:128).

According to the 2023 OBS:

- Only 3 countries—South Africa, Uganda and DRC— publish an IYR on a monthly basis, and within one month of the period covered (according to best practice);

- Parliamentary committees in 3 countries—South Africa, Benin and Zimbabwe— examined in-year implementation on at least one occasion during the fiscal year, and it published reports with findings and recommendations.

Second, legislatures should provide oversight of major changes to the enacted budget during budget execution. Such changes are typically presented and explained in a Mid-Year Review and approved by Parliament as part of a supplemental budget. Good practice indicates that legislatures should authorize the types of changes described below. Further, according to the IMF, supplementary budgets should be approved at fixed times of the year and no more than twice a year (more frequent use of supplementary budgets is an indication of a poorly prepared budget and weak budget execution (https://www.imf.org/external/pubs/ft/expend/guide4.htm )

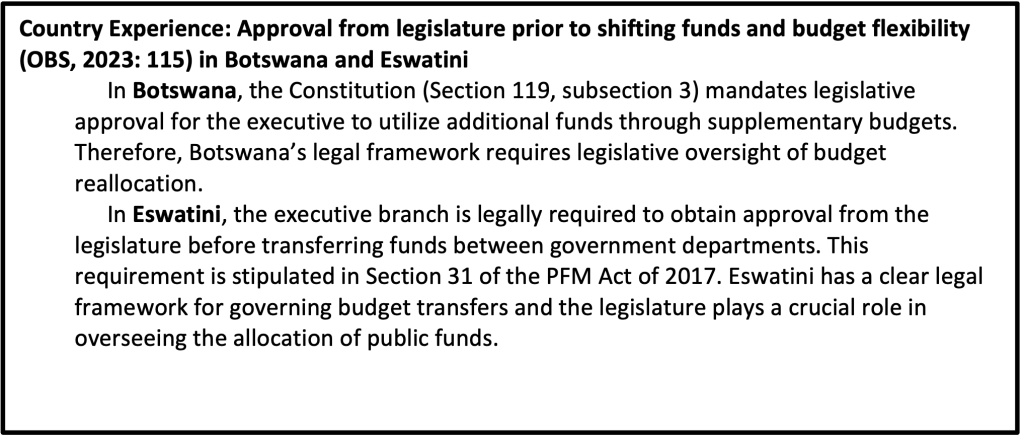

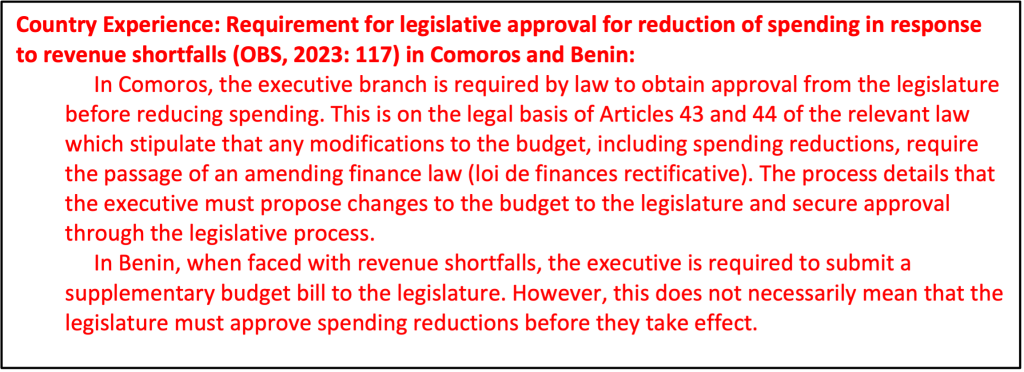

Here are three instances in which MoF should be returning to Parliament following approval of the EBP (OBS, 2023: 114):

1. Shifts in spending between administrative units: In most countries, the executive branch has some flexibility to shift spending between ministries and departments; however, to promote accountability, the executive should seek legislative approval before making major changes to the budget (e.g., shifting funds between administrative units) (OBS 2024b:130-131). Failing to do so can weaken the budget process and undermine legislative oversight provided during the approval process.

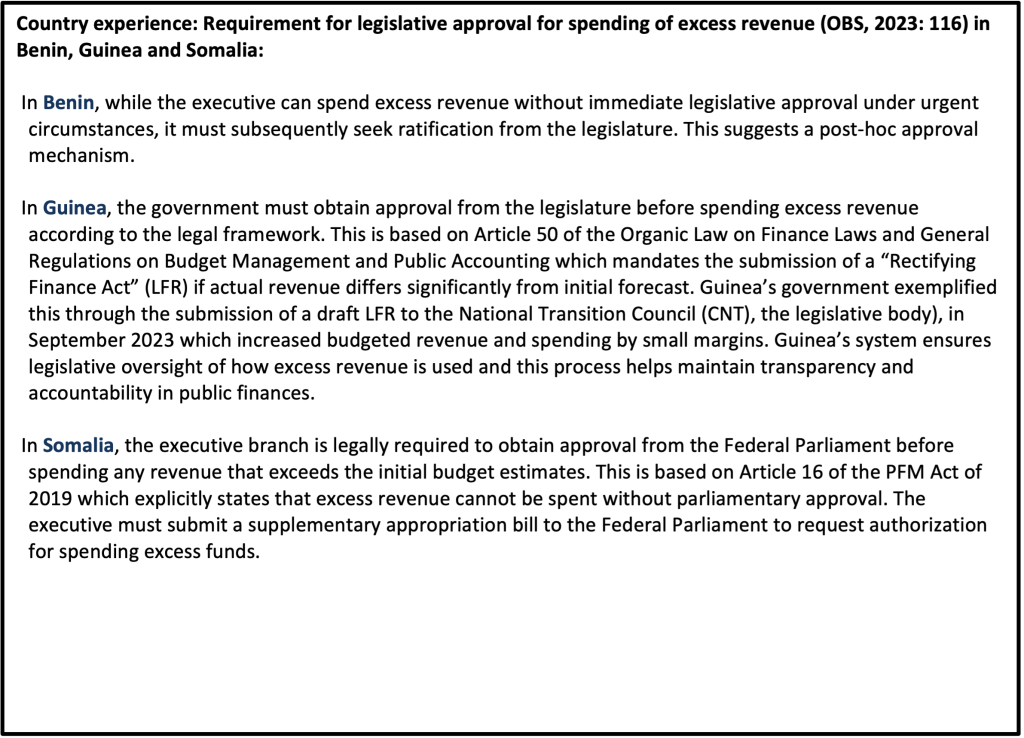

2. Authorize spending excess revenue: The executive branch should seek legislative approval before spending excess revenue. If such a requirement is not in place, the executive branch may have an incentive to underestimate revenue in the budget proposal to have the discretion to spend additional resources without legislative oversight (IBP 2024b:130).

3. Authorize reductions in spending below levels in the Enacted Budget: Similarly, the executive branch should seek legislative approval before reducing spending in response to lower than anticipated revenues. Such a requirement may be set out in the relevant laws or regulations, such as a public finance act. Without it, the executive branch has the discretion to substantially change the composition of the budget with no legislative control (IBP 2024b:131). Reductions in spending are often approved as part of supplementary budget, which is typically presented by the MoF, scrutinized in budget or finance committee, and approved in plenary. While examining the supplementary budget, committee members may request finance ministry officials attend hearings to respond to questions.

Third, parliamentarians can also call for greater transparency, especially during budget implementation. Subsequent rounds of the OBS have shown that budget transparency is stronger during budget formulation and approval compared to budget execution and oversight. For example, only 17 of the 41 countries in Sub-Saharan Africa assessed in the OBS 2023, published IYRs in a timely manner, compared to 34 of 41 countries publishing the Enacted Budget. Further, only 14 of the 41 countries published a Mid-Year Review in a timely manner.

These types of gaps in budget execution information, including the lack of justifications for budget deviations, are a key challenge impeding parliamentary oversight of budget implementation and can prevent parliament and other stakeholders from understanding budget credibility challenges. Research by the International Budget Partnership has shown that higher budget transparency is associated with better budget credibility (IBP 2022:44)

Legislative Scrutiny during the Audit/Oversight Phase

The Role of Supreme Audit Institutions (SAIs)

- At the end of the budget year, after all expenditures have been completed and recorded, the executive prepares a Year-end Report that shows total annual expenditures by agency (IBP 2008:102). The information in this report is verified by the SAI for accuracy and an audit report is submitted to the legislature, which in turn examines the audit report and seeks ‘corrective action’ from the executive (ibid). This section explores this process in more detail.

- SAIs play an important role in the budget process. SAIs are formal oversight institutions, which “protect the public interest by determining if budget decisions proposed by the executive and approved by the legislature are implemented as intended and deliver results (IBP 2022:37).” SAIs typically perform three basic types of audits (IBP 2020:59):

- Financial audits, which gauge whether the government’s financial accounts are accurate and reliable (free from errors or fraud) and which are submitted to the legislature for review during the oversight phase;

- Compliance audits, which verify whether public funds have been spent according to relevant laws and regulations; and

- Performance audits, which assess whether spending is efficient and effective.

- To provide effective oversight, SAIs require an institutional framework that provides them with adequate independence and resources. This includes (OBS 2024b:133-135):

- Legal independence in the appointment or removal of the head of the institution (that is, the legislature or judiciary, rather than the executive, authorizes such action providing the SAI independence from the executive).

- SAI’s budget is determined by an entity other than the executive (that is, by the SAI itself or by the legislature or judiciary).

- The SAI has the legal mandate to undertake the audits it wishes to in accordance with the applicable financial reporting and regulatory framework.

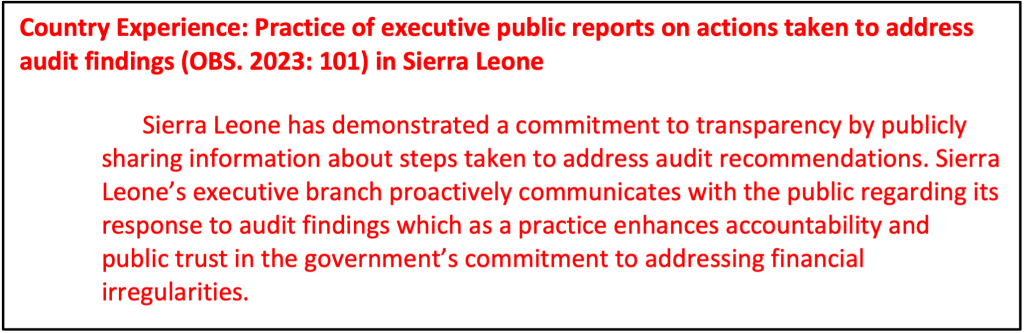

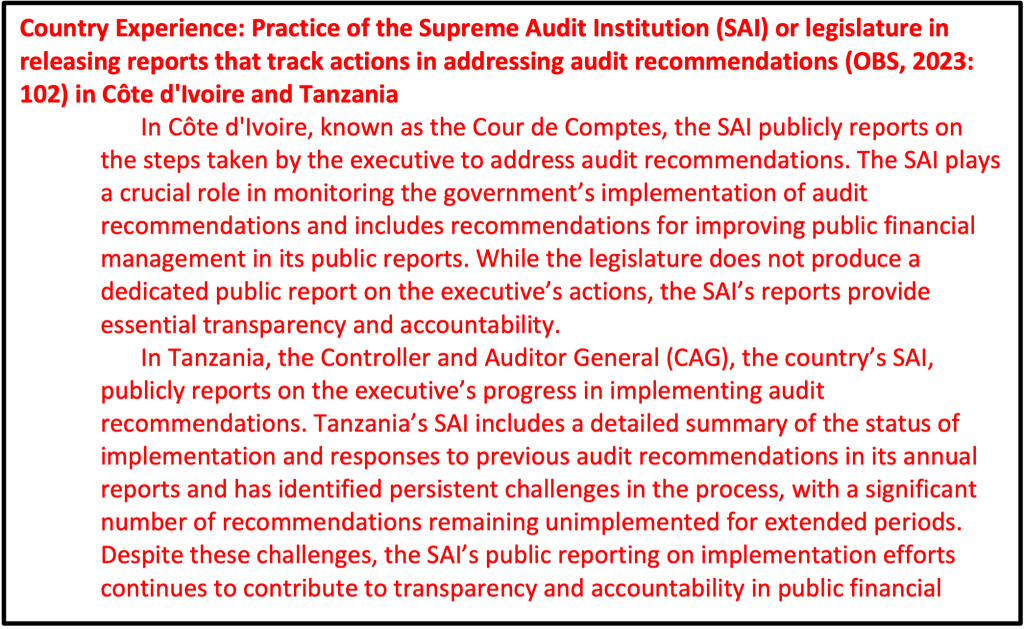

For SAIs to be effective, executives must respond to audit recommendations (OBS 2022:37).

‘Dynamic interaction’ between legislatures and SAIs is critical to pressuring executives to implement audit recommendations and report on their progress (ibid). After the SAI submits the financial audit report to the legislature, a legislative committee should examine the Audit Report on the annual budget (IBP 2024b:132).

As part of this process, the committee may hold public hearings where members of the executive are asked to testify regarding specific findings. After completing its review, the committee should produce and publish an official report with findings and recommendations, which may be debated and approved by the full legislature (IBP 2008:111).

However, follow-up is often lacking, with legislative committees in nearly one-half of the 125 countries assessed by the OBS failing to examine the Audit Report. Further, in nearly six out of ten countries, neither the legislature nor the SAI publicly track whether the executive has taken actions to address audit recommendations. In Sub-Saharan Africa, follow-up is even more rare. In a staggering 8 out of 10 countries, neither the legislature nor the SAI publicly track the executives progress on implementing audit recommendations.

- Exceptions, however, do exist. For example, the National Audit Office in the United Kingdom has an online tool to track the Executive’s progress on implementing audit recommendations (IBP 2022: 37). The Tracker is updated every six months and includes information on whether the government has accepted recommendations, the current state of implementation progress, and the departments responsible for implementation. The tracker is designed to be an interactive tool that allows users to explore the dataset in different ways.

Public Participation with SAIs during the Audit Phase:

- Increasingly, auditors are recognizing the value of public engagement both during the planning of the SAIs audit agenda as well as during audit investigations (IBP 2024: 40). According to the OBS 2023, auditors in 44 percent of surveyed countries have mechanisms in place for the public to provide input on the audit program. For example, in Ghana, the SAI has established a mobile app that allows citizens to provide input into audit planning, while in Romania the SAI provides clear instructions on its website on how the public can make submissions to inform the annual audit program (IBP 2022:29).

- While less common, auditors in 21 percent of surveyed countries have established mechanisms for public participation in audit investigations (up from 17 percent in the previous OBS) (IBP 2024: 40). For example, in the Philippines, the Commission on Audit (COA) has adopted the Citizen Participatory Audit, a mechanism whereby citizens and civil society organizations conduct audits as part of COA teams.

- Civil society can also ally with SAI to increase government responsiveness to audit recommendations. Working with SAIs, the media, and other civic actors, civil society can call attention to audit recommendations, prompting government action on recommendations that have been ignored (IBP 2022: 38)

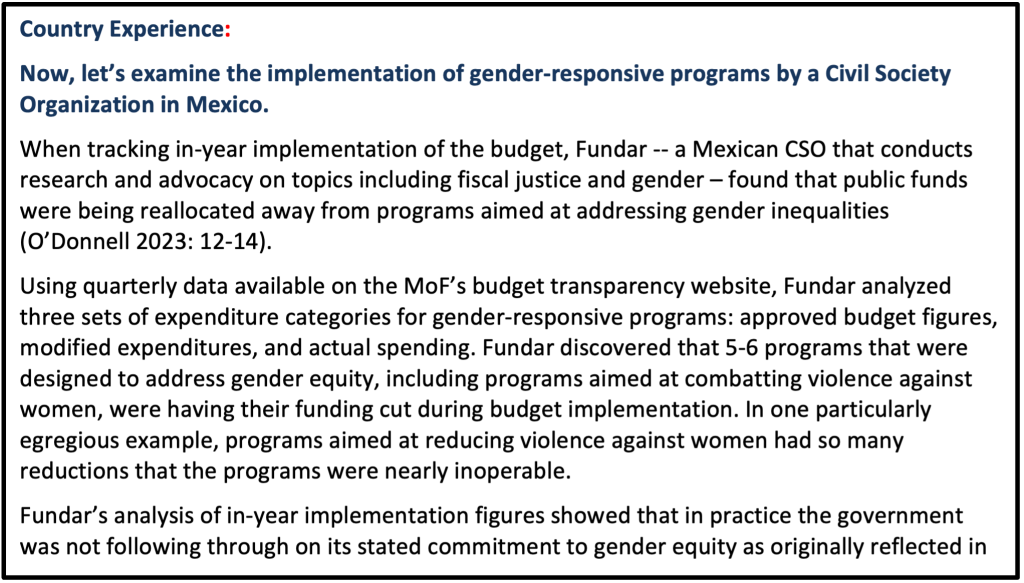

Role of Supreme Audit Institutions (SAI) in GRB:

- SAIs can undertake gender-responsive audits which can promote gender-responsive budgeting and policies in the following ways:

- Highlight compliance: Assess adherence to national and international gender equality commitments.

- Identify gender impacts: Examine effects of government programs on gender equality and equity.

- Recommendations for improvement: Provide insights to enhance policy design and implementation for better gender outcomes.

- Performance audits assess how well governments meet their gender equality commitments and how their programs impact different genders.

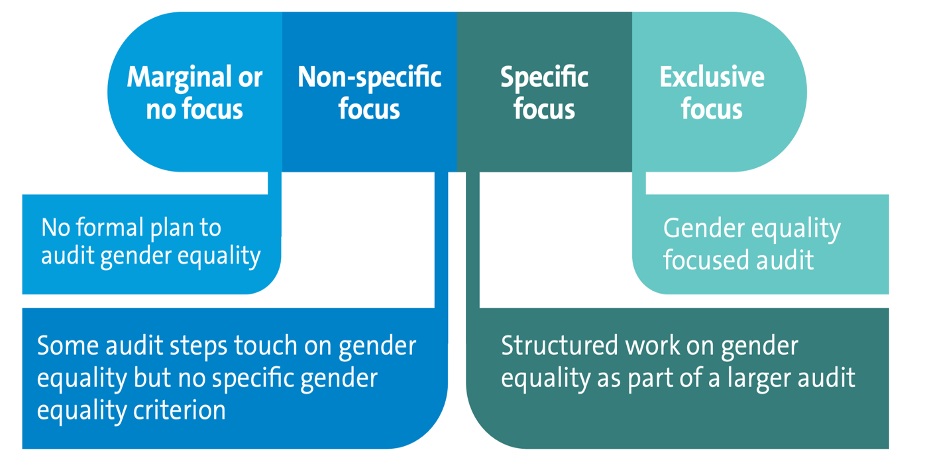

- These audits provide recommendations to improve policies and achieve better gender equality outcomes. Levels of Gender Focus in Performance Audits are (Deveaux and Dubrow: 2022):

- Marginal or No Focus: No formal plan to audit gender equality, but gender issues may arise during the audit;

- Non-Specific Focus: Some steps in the audit consider gender equality, even without specific gender criteria;

- Specific Focus: Formal gender audit is included as part of a more extensive audit;

- Exclusive Focus: The entire audit is specifically centered on gender issues.

By varying their focus on gender, performance audits can play a critical role in enhancing gender equality in government policies and actions.

- In addition, legislative committees can undertake reviews of any gender-responsive audits conducted by the SAI. In Austria, for example, the Court of Audit conducts gender equality audits, which are subject to scrutiny by the Audit Committee in parliament and facilitate parliamentary discussions on how to promote gender equality.

Gender-responsive audits can also be helpful in creating a record of where governments have fallen short with respect to promoting gender equality. For example, in 2015, the Canadian Office of the Auditor General (OAG), conducted an audit on whether the government adequately implemented gender-based analysis plus (GBA+) to inform government decision-making. The audit found that significant barriers remained to implementing the GBA+ framework and included a set of findings and recommendations, thus creating a record of where the government was falling short.

In 2022, the OAG conducted a follow up audit to examine whether the government had implemented recommendations from the earlier 2015 report. The follow-up audit documented the remedial steps the government had implemented as well as areas where it failed to make sufficient progress. The 2015 report, for instance, found that a lack of disaggregated data was a serious impediment to the application of the GBA+ framework. The 2022 audit highlighted that the original recommendation had not been fully implemented and recommended again that relevant departments work to ensure the use of disaggregated data in the design, delivery, and measurement of programs.

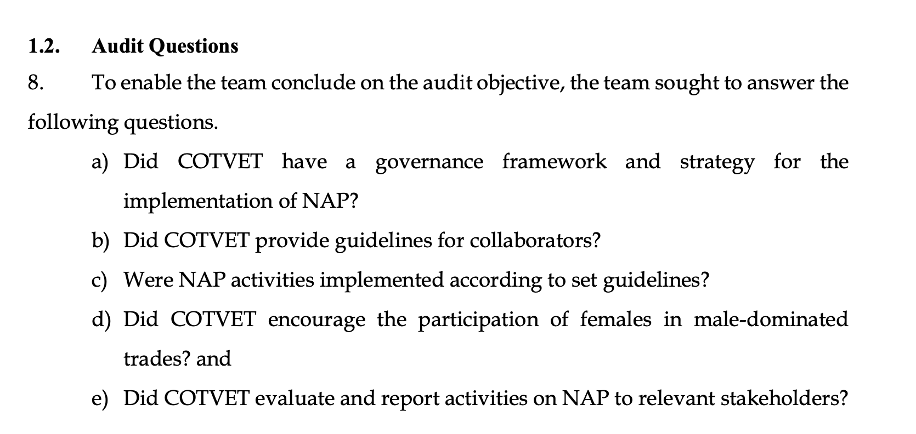

Pop Quiz: Levels of Gender Focus in a Performance Audit:

Background: Audit questions help auditors determine if specific objectives have been met. Gender-responsive audits can vary in their focus, from marginal to exclusive, as illustrated in the diagram that was just displayed.

Review the audit questions below from an excerpt of a performance audit:

Write the correct response in the comment box below

Leave a Reply

How would you characterize the levels of gender focus in this performance audit:

A) Marginal or no focus: No formal plan to audit gender equality.

B) Non-specific focus: Some audit steps touch on gender equality but with no specific gender equality criterion.

C) Specific focus: Structured work on gender equality as part of a larger audit.

D) Exclusive focus: A gender equality-focused audit.

Leave a Reply

The Role of Public Accounts Committees (Westminster system)

- In parliaments that are based on the Westminster political system, which originated in the UK, the public accounts committee (PAC), an ex-post committee of the legislature, will hold hearings to examine the Audit Report on the annual budget produced by the SAI. PACs will generally call the accounting officer — the most senior civil servant in a department — to account for deficiencies found in SAI reports. Best practice is for a legislative committee to have examined the annual Audit Report within three months of it being released by the SAI. PACs can be found in many Sub-Saharan African countries, including: Ghana, Kenya, South Africa, Tanzania, Zambia and Zimbabwe.

- Notably, many parliaments, including those in Ethiopia and Rwanda, which do not stem from the Westminster tradition, have also PACs.

- According to best practice, PACs will issue a report on its hearing, containing recommendations for the audited ministry, department, or agency (MDA) to address unresolved audit findings.

- PACs are expected to recommend that Parliament adopt recommendations that either endorse the auditor’s findings or add new recommendations based on committee hearings.

- The government typically provides a response to any PAC or committee report within a specific number of days, outlining the steps it has taken to address audit recommendations or findings requiring remedial action.

- The executive branch should make these responses publicly available, ensuring transparency in the follow-up to audit recommendations.

Oversight in Cour des Comptes System

The Cour des comptes system is particularly prevalent in Francophone and Lusophone Africa and is rooted in the Napoleonic model. It functions as the SAI with both judicial and administrative authority.

In Francophone Africa, countries such as Senegal, Ivory Coast (Côte d’Ivoire), Mali, and Cameroon have established a Cour des comptes. In Lusophone Africa, Angola and Mozambique have adopted the Cour des comptes model.

The Cour des comptes plays a critical role in auditing the financial management of public funds across various government bodies, including ministries, public agencies, and social security organizations.

Unlike the Westminster system, where the SAI reports directly to Parliament, the Cour des comptes in these countries does not automatically submit its reports to Parliament.

However, there are mechanisms for collaboration, such as:

- The president of the court passing findings to parliamentary committees.

- Parliament requesting specific audits.

- The court’s autonomy is reinforced by its status as a judicial body, ensuring that its magistrates can operate without external interference.

- The Cour des comptes holds significant enforcement powers, including:

- Issuing binding judgments on the recovery of public funds.

- Imposing fines.

- Mandating corrective actions for financial mismanagement.

-

November 21, 2024 7:04 pm

what is budget credibility?

The ability of governments to precisely and reliably meet their revenue and spending goals is referred to as budget credibility. It’s about honoring government pledges and comprehending the reasons behind their breakage1.What Makes Budget Credibility Vital?

Credibility of the budget is essential because:

Trust and Accountability: Public trust and accountability are increased when governments adhere to their budgets.

Service Delivery: Precise budgeting guarantees the timely provision of vital services, such as healthcare and education.

Economic Stability: Regular budgeting guards against unforeseen deficits and helps preserve economic stability.How is it relevant?

Credibility of the budget and my organization

Credibility of the budget is equally crucial to the mission of my organization:

Donor Trust: We must demonstrate to donors that they are capable of handling money in an efficient and open manner.

Project Success: Precise budgeting guarantees the successful completion of projects without incurring financial -

November 29, 2024 2:29 am

Budget credibility is about Government’s ability to deliver what it set out to do. It is a measure of the extent to which the expenditure was done as planned

-

November 29, 2024 3:03 am

B. Non specific focus

-

November 30, 2024 3:59 pm

Qu’est-ce que la probabilité budgétaire ?

C’est une situation dans laquelle existe des risques que les prévisions budgétaires ne puissent pas s’accomplir telles que prévues d’où la nécessité des poser des hypothèses de la survenance des risque et envisager les mesures d’atténuations pour y faire face

Pourquoi est-ce important ?

Car la survenance des risques budgétaires sans prévoir des mesures d’atténuations peut compromettre la réalisations des actions et priorités dégagées dans le budget de l’EtatEn quoi la fiabilité budgétaire est-elle pertinente pour votre mission organisationnelle ?

Elle permet d’avoir un budget réaliste conforment aux engagements pris vis à vis des citoyens -

December 4, 2024 10:43 am

Budget credibility refers to the extent to which a government’s budget reflects realistic, achievable financial goals and its ability to meet those goals. In other words, it is the degree to which a government can design and implement a budget that is both financially sound and executable. It involves ensuring that the revenue projections, expenditure forecasts, and fiscal policies laid out in the budget are credible and consistent with the government’s capacity to collect revenues and manage its spending.

Importance of Budget Credibility:

Financial Stability: Credible budgets contribute to fiscal discipline, reducing the risk of deficits or borrowing beyond a manageable level. They help prevent debt accumulation, ensuring long-term financial stability for the country.Investor Confidence: Credible budgets signal to investors that the government is financially responsible and capable of managing its finances, which can lead to lower borrowing costs and increased investment. On the other hand, if a government has a history of failing to meet its budget targets, it may face higher borrowing costs or lose access to certain capital markets.

Public Trust: When a government consistently meets its budget projections, it fosters trust with citizens and stakeholders. A lack of budget credibility, such as underestimating deficits or overestimating revenue, can lead to dissatisfaction, reduce public confidence, and undermine the government’s legitimacy.

-

December 4, 2024 11:20 am

In a performance audit, the level of gender focus refers to how gender considerations are integrated into the evaluation of public programs, projects, or policies. A performance audit assesses the efficiency, effectiveness, and economy of government activities, and introducing a gender lens helps ensure that the outcomes of these activities address the needs of all segments of the population, including different genders.

The levels of gender focus in a performance audit can vary depending on the depth of analysis and the specific gender-related objectives of the audit.

-

December 4, 2024 11:22 am

Indepth insight.

-

December 4, 2024 2:41 pm

1. Qu’est-ce que la crédibilité budgétaire ?

La crédibilité budgétaire fait référence à la confiance que les acteurs économiques ( Investisseurs, Entreprises et citoyens) accordent à la capacité d’un gouvernement à gérer ses finances publiques de manière responsable et transparente. En d’autre termes, elle fait référence à la mesure dans laquelle le budget d’un gouvernement reflète des objectifs financiers et économiques réalistes, atteignables ou réalisables.

Pourquoi est-ce important ?

La crédibilité budgétaire est importante dans la mesure où elle assure i)la transparence: Un gouvernement crédible publie des informations claires et accessibles sur ses finances, y compris les prévisions budgétaires , les dépenses et les recettes. ii) Responsabilité: cela implique que le gouvernement respecte ses engagements budgétaires et qu’il est tenu responsable de ses décisions économiques. iii) Garanti la stabilité économique: la crédibilité budgétaire est liée à la stabilité économique d’un pays. Un cadre budgétaire stable contribue à la confiance des investisseurs et à la prévisibilité des politiques économiques. iv) Assure une politique budgétaire cohérente car un gouvernement qui adopte des politiques budgétaires prévisibles et cohérentes sur le long terme est perçu comme crédible. v) Anticipe les réactions aux chocs, la capacité d’un gouvernement à réagir de manière appropriée aux crises économiques renforce sa crédibilité. car une gestion efficace des imprévus budgétaires montre une bonne gouvernance.

La crédibilité budgétaire est essentielle pour maintenir la confiance dans les institutions publiques et favoriser un environnement économique stable et attractif.

3;Dans quelle mesure la crédibilité budgétaire est-elle pertinente pour la mission de votre organisation ?

Comme nous l’avons dit plus haut la crédibilité budgétaire est pertinente pour la mission de notre organisation dans la mesure où elle nous permet de bâtir des évidences pour une plus grande transparence budgétaire et d’établir un sentiment de confiance ou de redevabilité des institutions publiques, et de pousser la participation des citoyens aux politiques publiques, . Elle nous permet de promouvoir la littératie budgétaire des citoyens pour un meilleur suivi de l’action publique. -

December 4, 2024 3:12 pm

D) Did COTVET encourage the participation of females in male dominated trades ?

-

December 5, 2024 8:28 am

Budget credibility – also known as budget reliability – can be simply understood as the ability of governments to meet the expenditure and revenue targets set out in their budgets accurately and consistently. Shortcomings around budget credibility affect government agencies at both the central and subnational levels. They can undermine evidence-based spending decisions, divert funds from originally agreed upon priorities and levels, and weaken parliaments’ capacities to hold budget execution agencies accountable. They are also closely linked to a country’s overall economic performance, macro-economic stability, and creditworthiness.

Budget credibility is important because they influence trust and accountability, effective planning and economic stability. Precisely, the credibility of a budget is linked to a country’s overall political economy, the level of fiscal transparency and accountability, and to the quality of PFM systems.

Budget credibility is important to my organisation as ensures that financial resources are available and managed properly to achieve organizational and societal goals. With this, we are able to project the key determinants/variants to take into account within existing legal framework.

-

December 5, 2024 9:08 am

B) Non-specific focus: Some audit steps touch on gender equality but with no specific gender equality criterion.

-

December 6, 2024 8:38 am

What is Budget Credibility?

Answer

Budget Credibility is an important cornerstone of good financial governance which is essentially defined as :

– the ability of government to uphold it’s commitments and consistently meet it’s revenue and expenditure targets.2. Why is it important?

– it is a key part of good financial governance and is a sign that government is upholding it’s commitments

– if budget are implemented as intended, this directly impacts when and how essential services are delivered and can undermine progress in addressing poverty and inequality.3. How is budget credibility relevant to your organizational mission?

Budget Credibility is relevant to my organization for the following reasons:

I) Transparency and Effectiveness

– as an organization we will ensure that resources are used transparently and effectively to achieve planned goals.

ii) Good Financial Governance

– resources under the organization’s purview will be handled under good financial governance polivy–

-

December 7, 2024 12:42 am

What is Budget Credibility?

Budget credibility refers to the reliability and accuracy of budget estimates, projections, and allocations. A credible budget is one that is based on realistic assumptions, accurately reflects the government’s policy intentions, and is implemented as intended.

Why is Budget Credibility Important?

Budget credibility is essential for several reasons:

1. Promotes Transparency and Accountability: A credible budget provides a clear picture of the government’s financial plans and priorities, enabling citizens to hold the government accountable.

2. Supports Effective Resource Allocation: A credible budget ensures that resources are allocated efficiently, reducing waste and misallocation.

3. Enhances Economic Stability: A credible budget helps maintain economic stability by providing a clear fiscal framework, reducing uncertainty, and promoting investor confidence.

4. Fosters Public Trust: A credible budget builds public trust in the government’s ability to manage public finances effectively.Relevance to CISLAC’s Organizational Mission

As a civil society organization focused on promoting transparency, accountability, and good governance in Nigeria, CISLAC’s mission is closely tied to the concept of budget credibility. By advocating for a credible budget, CISLAC can:

1. Promote Transparency and Accountability: CISLAC can push for budget transparency, ensuring that citizens have access to accurate and timely budget information.

2. Support Effective Resource Allocation: By analyzing budget allocations, CISLAC can identify areas of inefficiency and advocate for more effective resource allocation.

3. Enhance Economic Stability: CISLAC’s advocacy for a credible budget can contribute to economic stability, promoting a favorable business environment and reducing poverty.

4. Foster Public Trust: By promoting budget credibility, CISLAC can help build public trust in the government’s ability to manage public finances effectively, ultimately strengthening democratic governance in Nigeria. -

December 8, 2024 12:49 pm

What is budget credibility?

This refers to the government’s capacity to stick to its approved budget in terms of both expenditures and revenues. It assesses whether actual spending and revenue collection match the plans set out in the approved budget. A credible budget indicates that the government is dependable in fulfilling its financial commitments and policy priorities.

Why is important?

Budget credibility reduces the chances of corruption and wastage of public resources and strengthens accountability and oversight. Citizens are more likely to trust the government when its financial commitments are fulfilled as planned, fostering confidence in governance ultimately improving service delivery.

How is budget credibility relevant to your organizational mission?

As an organization that advocates for increased funding to essential services like health and education, budget credibility ensures that the allocated resources are delivered and used as intended. Advocacy efforts rely on consistent and effective government spending. Monitoring and evaluating government budget execution requires credibility to identify deviations and push for improvements. Without credibility, measuring impact and demanding accountability becomes challenging.

-

January 12, 2025 2:44 pm

La crédibilité budgétaire est le processus ou ,les règles de respect dans l ‘exécution du budget afin que les ressources collectées financent exactement les besoins précis des populations au cours d’une année.

Il est important pour assurer le développement des infrastructures et le financement précis des biens ou services des populations. Il permet d ‘éviter la corruption.

La crédibilité budgétaire est important et pertinent pour notre mission car elle nous permettra de suivre l ‘exécution du budget mais aussi surveiller et assurer le contrôle. -

January 12, 2025 3:07 pm

La crédibilité budgétaire est la capacité du gouvernement à gérer les fonds publics. Elle instaure la confiance des investisseurs, des prêteurs et renforce l ‘image du gouvernement envers la population.

-

January 26, 2025 12:36 am

**Budget credibility** is how well actual outcomes match the planned budget.

**Importance**: Ensures efficient use of resources and accountability.

**Relevance*: Ensures resources are allocated to meet organizational goals.

Leave a Reply